The Coronavirus Aid, Relief, and Economic Security (CARES) Act is an economic relief bill that is pumping $2.2 trillion into the economy to counter act the affects the pandemic has had on our economy. The intent is to help individuals and businesses who have economic hardships due to the virus. There are three main ways the CARES act could give you and your family economic relief.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act is an economic relief bill that is pumping $2.2 trillion into the economy to counter act the affects the pandemic has had on our economy. The intent is to help individuals and businesses who have economic hardships due to the virus. There are three main ways the CARES act could give you and your family economic relief.

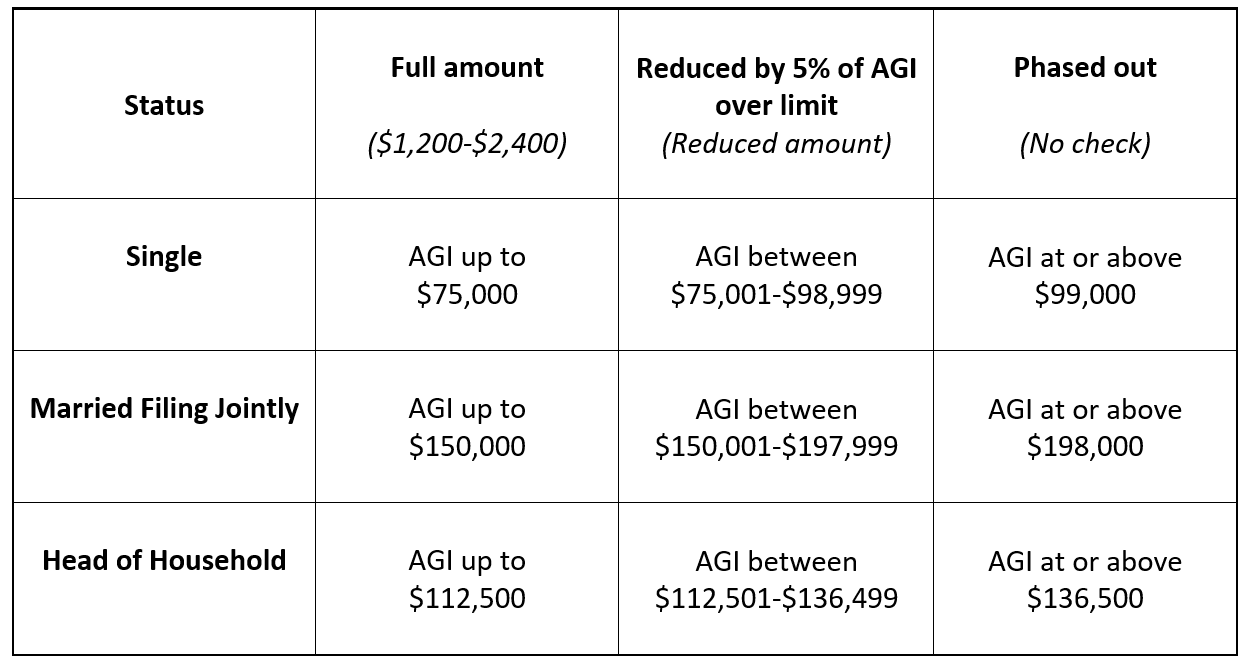

You May Receive a Stimulus Check

Approximately $300 billion will be distributed to citizens through checks of up to $1,200. How much you will receive depends on your Adjusted Gross Income (AGI) from 2019. If you did not file income taxes in 2019, your AGI from 2018 will be used. Single filers with an AGI of $75,000 or less (or $112,500 for individuals filing as Head of Household) can expect to receive the full $1,200 check. Married people filing jointly with a joint AGI of $150,000 or less can expect the full $2,400. The amount of the stimulus checks starts to be phased out at these limits and is phased out all together at $99,000 for single filers, $136,500 for head of household, and $198,000 for married filing jointly.

For those making between the limit for the full amount and the phased-out amount, the check will be reduced by 5% of the amount over the AGI limit. For example, if you are a single filer with an AGI of $90,000, you are over the $75,000 amount by $15,000. 5% of $15,000 is $750. You would receive a check for $450 ($1,200 – $750).

If you are set up for direct deposit with the IRS, your money should be delivered to your account by April 17th, 2020. If you have recently set up direct deposit or receive paper checks, it could come later. An exact date has not been given.

What about children?

Parents with qualifying children age 16 or under listed as dependents on their 2019 tax return will receive an additional $500 per child.

Children or college students under age 24 who are listed as dependents should not expect to receive anything.

What if I wasn’t eligible in 2019 but am now?

If you are not eligible based on your 2019 tax return, but you would be based on your 2020 income, you may receive a tax credit when you file your tax return for 2020.

Do I need to apply?

No, the IRS will automatically send you a check or direct deposit the money in your account based on your 2019 tax return.

What if I didn’t file taxes?

If you would qualify but did not file taxes for 2018 or 2019 you must file a simple tax return to receive payment. If you are confused or concerned about filing, contact a tax professional.

More People are Eligible for Unemployment

Unemployment has been expanded to include more people than ever before. It includes benefits for the self-employed and part time workers as well as fully unemployed people. Almost anyone who is unemployed, partially unemployed, or unable to work for coronavirus-related reasons is eligible for benefits.

Unemployment checks will also be higher than normal. The amount varies by state. In Wisconsin a weekly unemployment check is typically 4% of your highest earning quarter, with a maximum of $370 per week. The stimulus package raises that by $600 per week making the maximum $970 a week. In addition, the maximum benefit period has been expanded by 13 weeks.

Forgo your Required Minimum Distribution (RMD) and Let your Money Grow

The CARES Act has waived the requirement to take a distribution from a retirement account. RMDs are calculated using the value of the account on December 31st of the previous year. Since most accounts have experienced a sharp decline this year, RMDs would represent a larger percentage of the portfolio. Typically, RMDs must be taken from retirement accounts such as IRAs, and 401(k)s every year starting at age 72 (or 70 ½ before 2019). In 2020, no distribution is mandatory. This allows people who are not using their RMDs to let their accounts recover untouched. If you are relying on your RMDs as a source of income, you may still take it. The act simply gives the individuals the choice. This is also true for inherited accounts.

If you are forgoing your RMD this year, it may be a good time to consider a Roth conversion. Moving money to a Roth IRA allows it to grow tax free. However, in the year you do the conversion, the amount converted is taxed. The taxes you pay for a Roth conversion are the same taxes you would pay had you taken an RMD.

Talk to a financial planner to decide if it is in your best interest to take a distribution, skip a year, or do a Roth conversion.